The cryptocurrency liquidity provider market is heading for a shakeout. This is the verdict of three-quarters of institutional OTC participants surveyed by crypto liquidity network Finaly Markets, whose new annual report calls 2026 the year consolidation pressures become impossible to ignore.

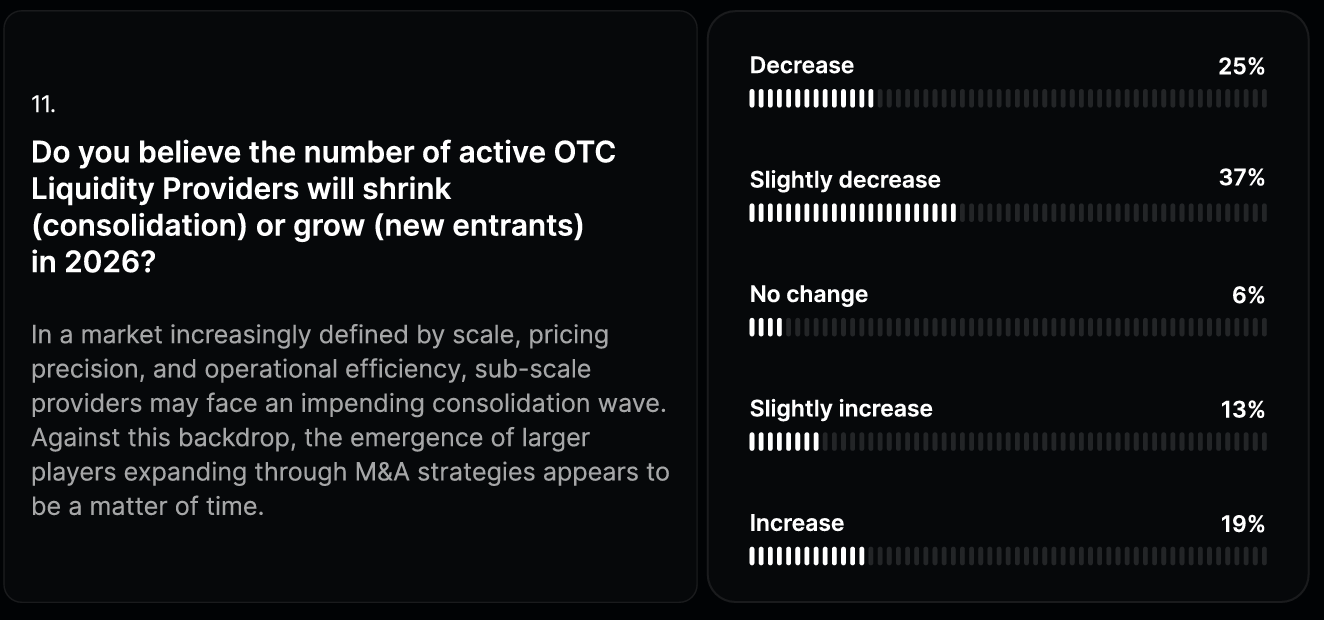

The number of liquidity providers is expected to decrease

Six in 10 OTC market participants expect the number of active liquidity providers to decline by the end of 2026, with 25% predicting a complete decline and a further 37% predicting a slight contraction. Only 32% of respondents expected new entrants to offset losses.

“In a market increasingly defined by scale, pricing accuracy, and operational efficiency, smaller providers may face an impending wave of consolidation,” the report said.

For CFD brokers that rely on a fragmented pool of cryptocurrency liquidity providers to power their pricing engines, fewer active market makers mean narrower competitive tensions on spreads, concentrated risk in liquidity sourcing, and lower negotiating leverage on execution quality.

B2Broker’s decision last November to connect its institutional crypto OTC services directly to Finery Markets’ ECN is an early example of how some companies are responding to this structural pressure.

The merger of Zodia Custody and Finaly Markets, announced in April 2025, similarly reflects a broader trend for institutional investors to build direct connections to electronic liquidity networks rather than going through traditional intermediaries.

Margin compression has already begun

The expected integration is not a hypothesis. Finery Markets revealed that 75% of companies surveyed reported a significant contraction in profit margins in 2025, half reported a decline in profit margins, and companies reported a slight decline in the quarter. Only 8% said it had improved.

Companies that can best withstand this pressure are those that invest in technology that replaces labor costs. Algorithmic pricing and post-trade automation each ranked as technology investment priorities for 2026 for 31% of those surveyed.

(#Highlighted link#)

This pattern will be familiar to anyone who followed the retail exchange industry through its unique compression cycle in the 2010s. The report itself draws a clear parallel, explaining that the current OTC crypto market reflects a structural shift towards electronic, regulated liquidity flows in the $9.6 trillion per day foreign exchange market. X Open Hub’s expansion of its institutional crypto OTC liquidity pool earlier this year reflects the same logic being applied to the situation facing CFDs.

$27 trillion lawsuit against Legacy Rail

The trapped capital figure is at the heart of the broader case the report makes about stablecoin payments. They argue that traditional SWIFT and SEPA infrastructure forces financial institutions to pre-deploy capital across multiple venues days before it is needed, creating a “fragmentation tax” for all companies that cannot rebalance in real time.

“The end of locked-up capital: An estimated $27 trillion remains locked up in pre-funded accounts in traditional railroads,” the report states. “Atomic payments (T+0) in the stablecoin era enable just-in-time liquidity, freeing up institutional capital for immediate redeployment.”

According to the report, the annual trading volume of stablecoins now exceeds $57 trillion, and the share of stablecoins in institutional OTC trading volume will increase from 23% in 2023 to 78% in 2025. On Ethereum and Layer 2 networks, transactions settle in less than a second and for less than a cent, compared to the 24-hour or more payment cycles common on traditional banking platforms.

FinanceMagnates.com reported in January that the adoption of stablecoins as payment tools at the broker level is increasing, forcing companies to adapt their back-office infrastructure accordingly. A separate analysis in June 2025 detailed how CFD brokers are specifically looking at stablecoins for cross-border payments, citing cost savings and settlement speed as key factors.