Bitfinex Securities announced on Monday that it has resumed issuance of tokenized bonds for Luxembourg-based securitization fund ALTERNATIVE and expects future sales to exceed $10 million.

USDt-denominated bonds are issued and settled on Bitcoin’s sidechain, the Liquid Network, with funding, coupon payments, and principal repayments occurring entirely on-chain.

The move follows four previous tokenized bond issuances totaling $6.2 million starting in 2023, three of which have matured and been repaid in full, returning approximately $1 million in principal to investors.

Through these offerings, investors received 20 on-chain coupon payments worth more than $1.1 million by the completion of the first full tokenized bond cycle in 2025, according to the companies. The bond provides investors with exposure to emerging market private credit, including lending to small and medium-sized enterprises and women-led businesses.

Bitfinex Securities operates under license from the Astana International Financial Center in Kazakhstan and El Salvador and handles issuance, listing and secondary trading, while Tether’s Hadron platform supports token management. The platform currently claims to have approximately $250 million of regulated tokenized securities listed.

Jesse Knutson, head of operations at Bitfinex, told Cointelegraph that buyers are primarily high-net-worth crypto investors and crypto institutions in Europe and Asia who are looking for yield on their USDt (USDT) holdings.

Tokenized bonds operate alongside an issuer’s traditional monthly bond program and typically have a tenor of 11 months. Transactions are recorded on Liquid Network, but key payment details are protected by confidential trading features.

He further added, “There has been a lot of discussion about yield-producing stablecoins this year. This product provides a solution with an easy, regulated and established means of earning yield from USDt balances.”

Related: Bitcoin exposes structural weaknesses that banks refuse to admit

Debate intensifies over yield vs. no yield

The reopening comes as debate continues over whether stablecoins should be allowed to offer yield and how such products should be regulated in the United States.

The passage of the US GENIUS Act in July 2025 prohibited stablecoin issuers from paying yield, but the law did not explicitly prohibit third parties from providing returns through another product. This “loophole” allowed exchanges and other third-party platforms to build yield-producing securities and loan products on stablecoins without the issuers themselves distributing the interest.

Banks have warned that high-yield stablecoin products could draw deposits away from the traditional financial system. Bank of America CEO Brian Moynihan said in January that interest-bearing stablecoins could drain up to $6 trillion in deposits from U.S. banks, arguing that a mass shift to digital dollar products could reduce lending capacity and increase funding costs.

The debate has become one of the most contentious issues surrounding the CLARITY Act, a US bill aimed at establishing a broader regulatory framework for digital assets. On January 14, Coinbase CEO Brian Armstrong withdrew his support for the bill, citing stablecoin yields as one of the key issues.

Still, some lawmakers remain optimistic. On February 18, U.S. Sen. Bernie Moreno said in an interview with CNBC from President Donald Trump’s Mar-a-Lago mansion in Florida that he expects Congress to advance a market structure bill by April. Armstrong, who was interviewed alongside Moreno, said he believed there was a path forward that “could get a win-win outcome here.”

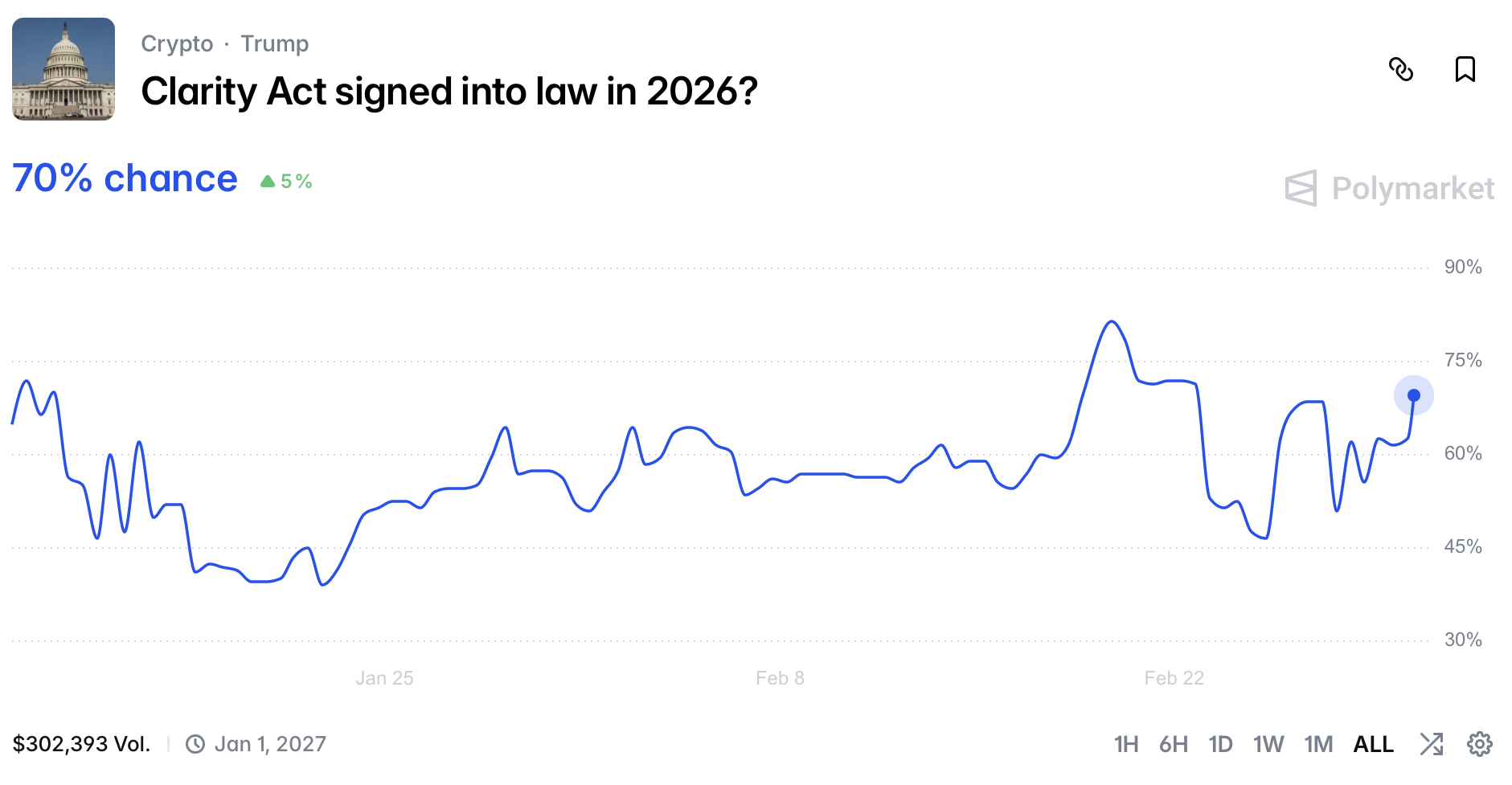

According to Polymarket’s predictive market data, the Clarity Act currently has a 70% chance of becoming law in 2026.

sauce: Polymarket

magazine: Crypto lawyer warns that transparency laws risk repeating Europe’s mistakes