Riot case study shows US Bitcoin miners can clear power costs long before earning full profits

Bitcoin mining costs are often reduced to a single number. $BTC”In reality, this number varies depending on which tier of your business you measure.

Power determines whether machines run today, operating costs determine whether the mining fleet supports the entire enterprise, and accounting costs determine whether the enterprise ultimately reports a profit.

To examine these layers more clearly, crypto slate built Bitcoin mining cost model We calculate mining economics based on first principles using network difficulty, block rewards, transaction fees, ASIC efficiency, and power prices.

The model then applies company-specific cost inputs using Riot Platforms’ public documentation to show how the real-world economics stack up.

In the current network situation, this model shows that while miners can cover electricity costs, they are still unable to cover extensive operational and accounting costs.

Riot’s Texas operations reveal just how far electrical breakeven, operating breakeven, and full accounting profitability can remain even after Bitcoin prices recover.

Riot’s mining economics reveals three break-even tiers

At the current Bitcoin price of $67,200, Riot has cleared one break-even tier and missed the next two.

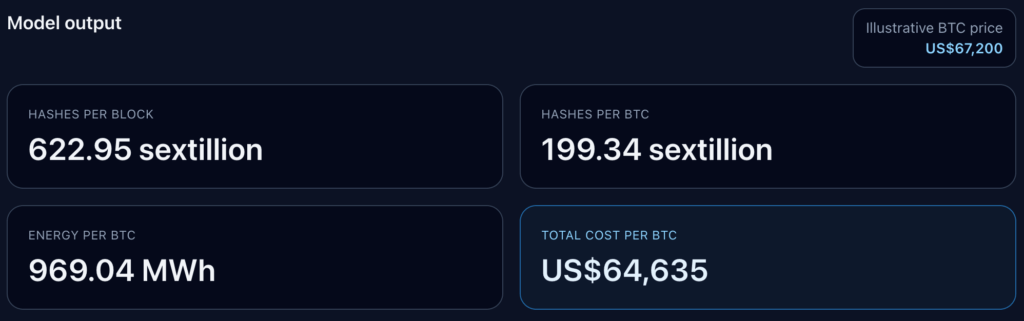

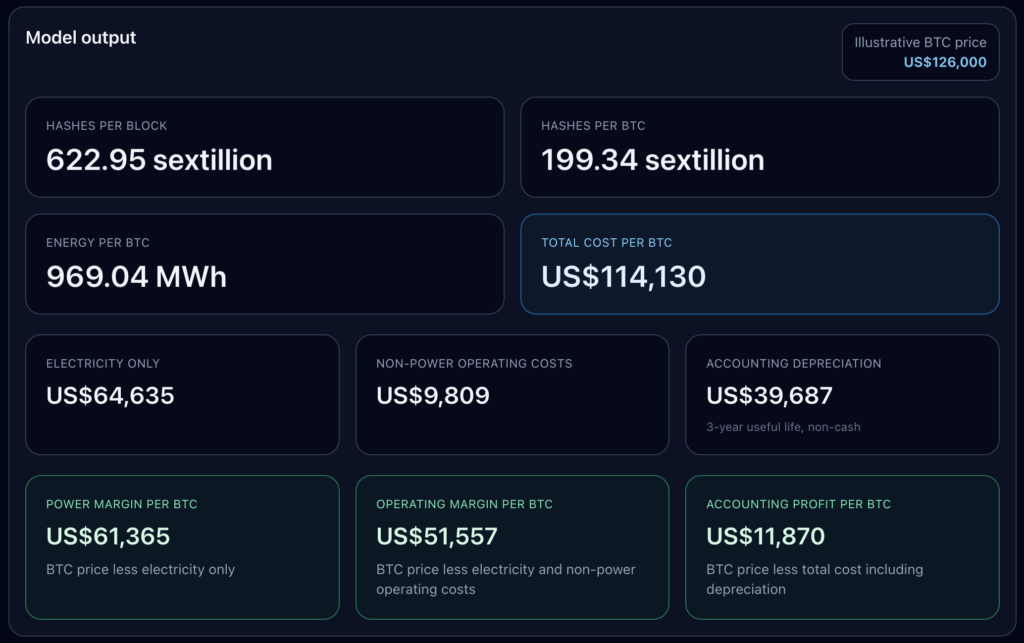

We modeled the data based on current network conditions, such as Bitcoin difficulty 145,042,165,424,850, 3.125. $BTC block reward, $BTC Per block, modern ASIC efficiencies range from about 17 to 19 J/TH, and industrial power in Texas costs about $0.0667 per kWh. We ignored block fees considering the current average is around 0.02. $BTC block by block.

This configuration generates a network total of 622.95 sextillion hashes per block (the total amount of work the network needs to do on average to mine one block) and 199.34 sextillion hashes per block. $BTC (the speed at which a miner or the entire network does its work), and 969.04 megawatt-hours of energy $BTC.

With these assumptions, the electricity cost for Mining 1 is $64,635. $BTC At current prices, the power margin is $2,565 per unit. $BTC.

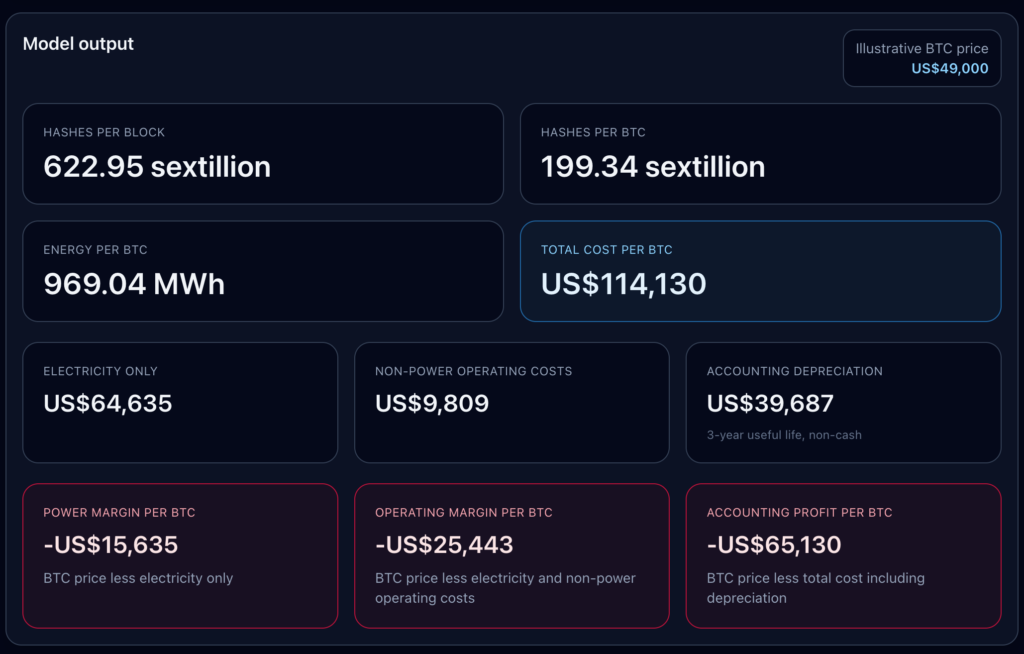

Add in Riot’s application-based non-power operating cost tier and you get about $9,809 per claim. $BTCthe operating margin was negative $7,243, and the total cost per case was $BTC Jump accordingly. Adds a non-cash depreciation layer of approximately $39,687 per item. $BTC Accounting profit is pushed to negative $46,930.

This clearly shows that for large-scale miners in the US, “the cost to mine one Bitcoin” is not a single number.

- One layer helps you understand short-term electrical costs and decide if it’s worth running the machine.

- The second layer adds broader operating costs and indicates whether self-mining covers the rest of the business.

- The third layer adds depreciation and shows whether reported profits are keeping pace with cash profits.

The model places these layers side by side and shows how far apart they remain after the market recovers.

Breakeven point ladder defines business situation

This model produces a break-even ladder that indicates more than a single all-in mining cost number. The break-even point for electricity only is $64,635 per case. $BTC.

Add in Riot’s application-based non-power operating cost tier and the break-even point rises to approximately $74,444.

Adding the accounting depreciation layer raises the complete accounting break-even point again to $114,130.

Therefore, miners can report positive power economics while producing weak operating and accounting results.

We modeled four pricing scenarios to show how that ladder works in practice.

In my $49,000 bear case, Riot is negative in every way. Power margin per $BTC is negative $15,635, operating margin is negative $25,443, and accounting profit is negative $65,130.

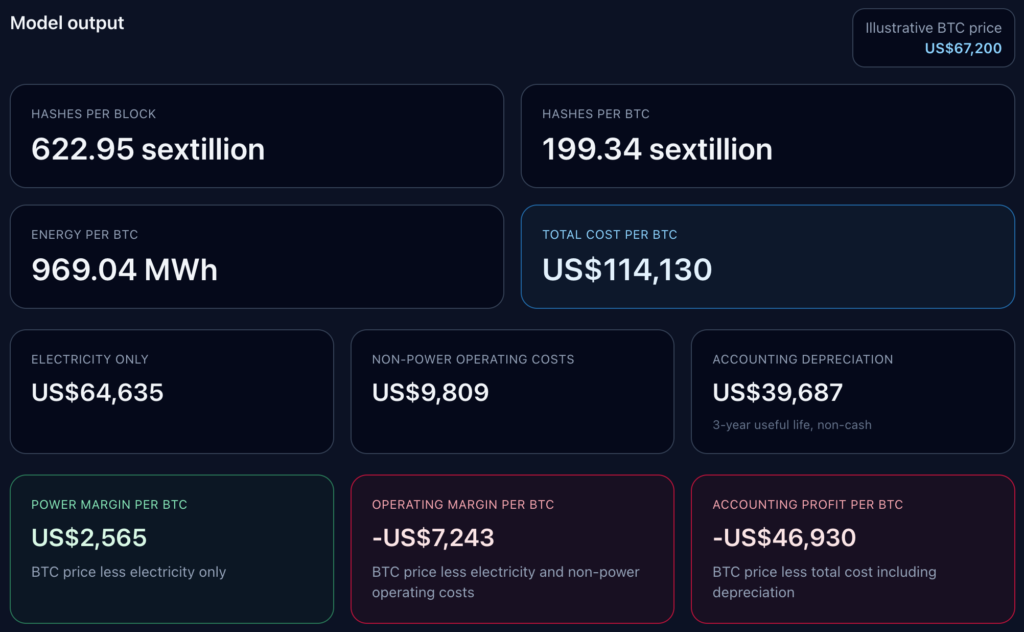

At the current price of $67,200, Riot is slightly above breaking even on electricity, but just barely. Power margins turn positive, but operating and accounting outlooks remain negative.

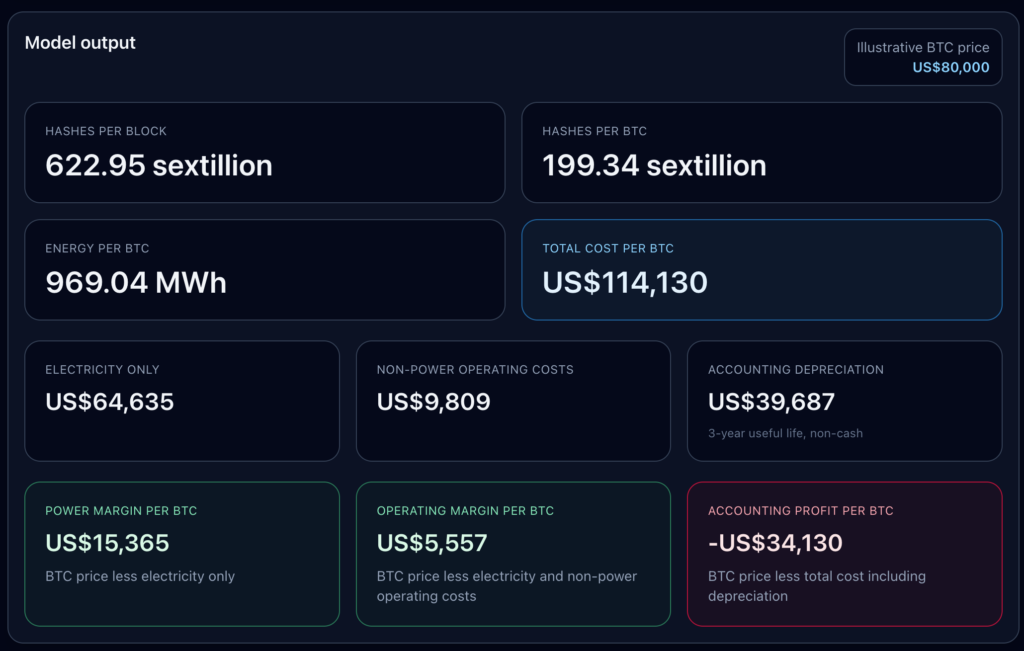

For the $80,000 collection cases, Riot passes the operating threshold with an operating margin of $5,557 per case. $BTCMeanwhile, the accounting view still shows a loss of $34,130.

For all three outlooks to be positive, the all-time high of $126,000 would have to be broken again, resulting in an accounting profit of $11,870 per deal. $BTC.

This difference is substantial. Riot’s depreciation layer is explicitly structured as non-cash and is based on a three-year useful life. This is an accounting allocation rather than a short-term avoidable cash out.

Public miners do not live solely on electricity margins, so this issue remains a consideration. They report income statements. They replace machines. They absorb corporate costs.

Therefore, a useful question is which profitability line are investors, analysts, and management teams actually using, and when do they consider a miner to be profitable?

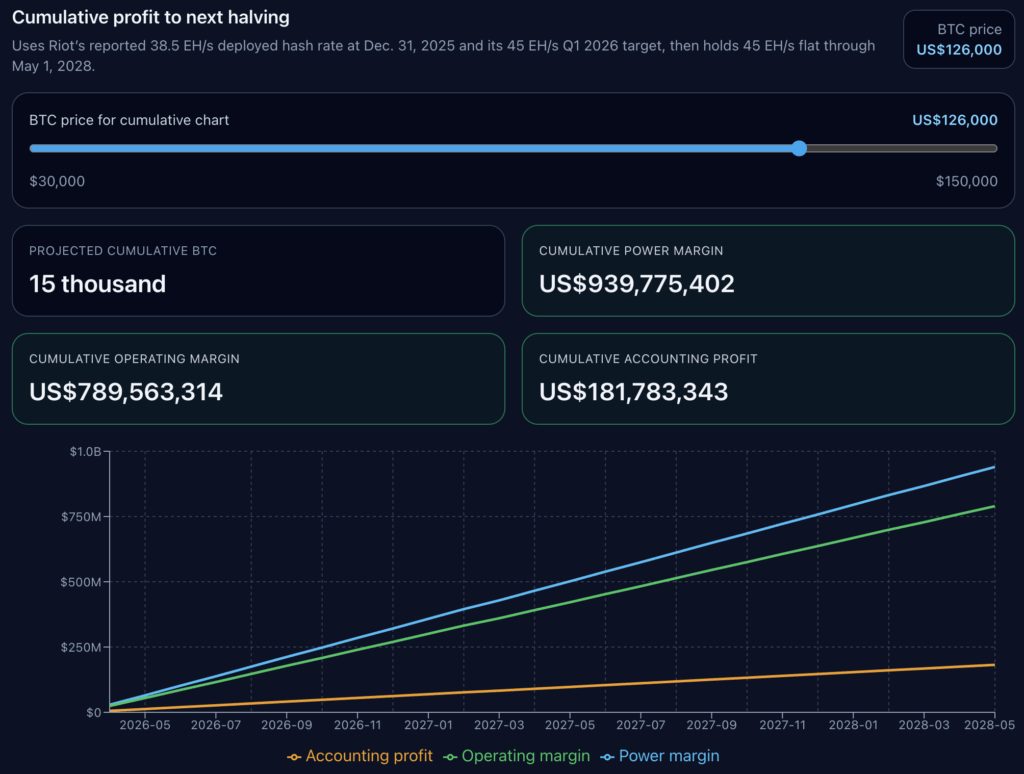

Riot’s Next Halving Prediction Extends Price Test

We then performed cost projections through the next halving in 2028.

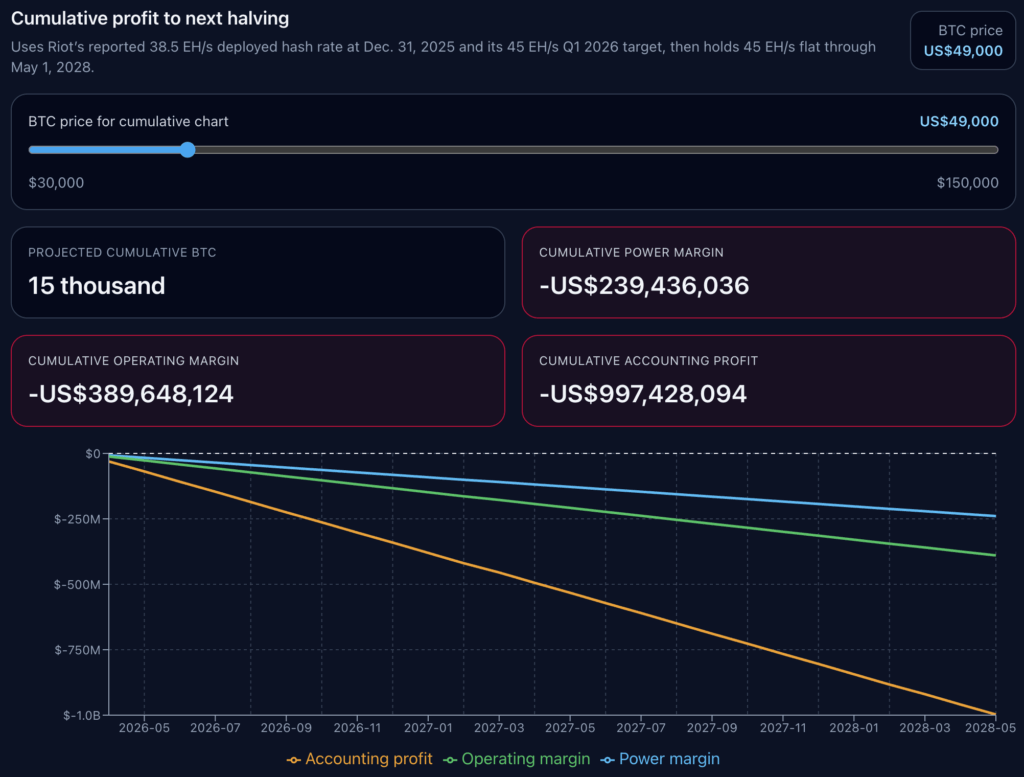

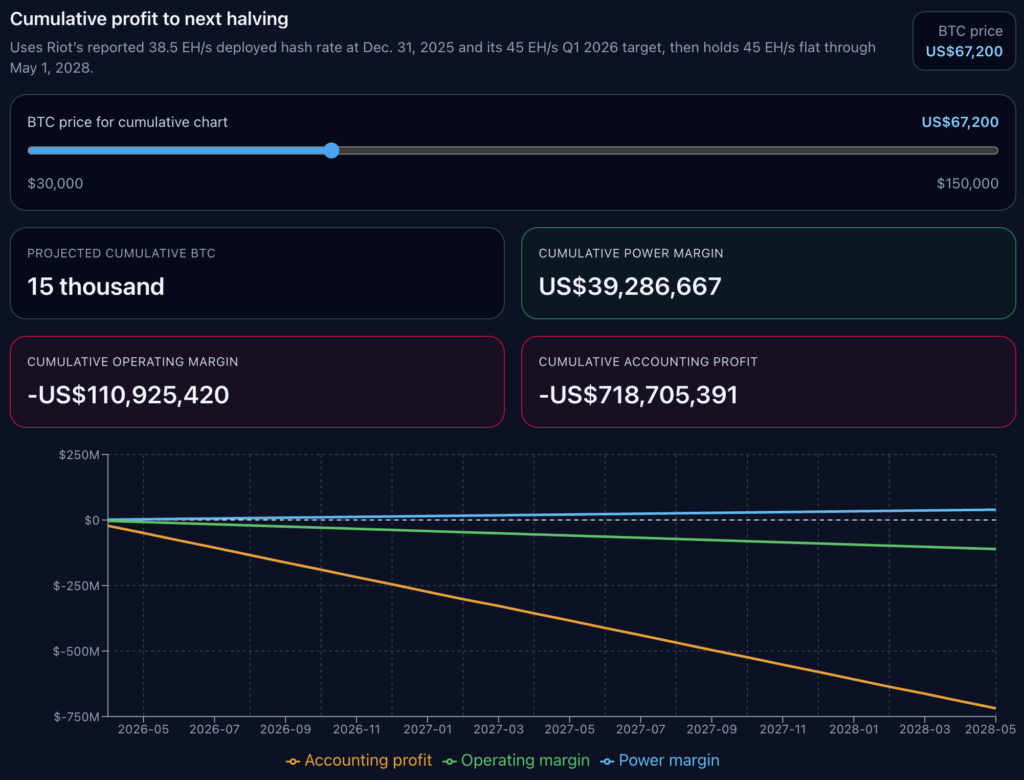

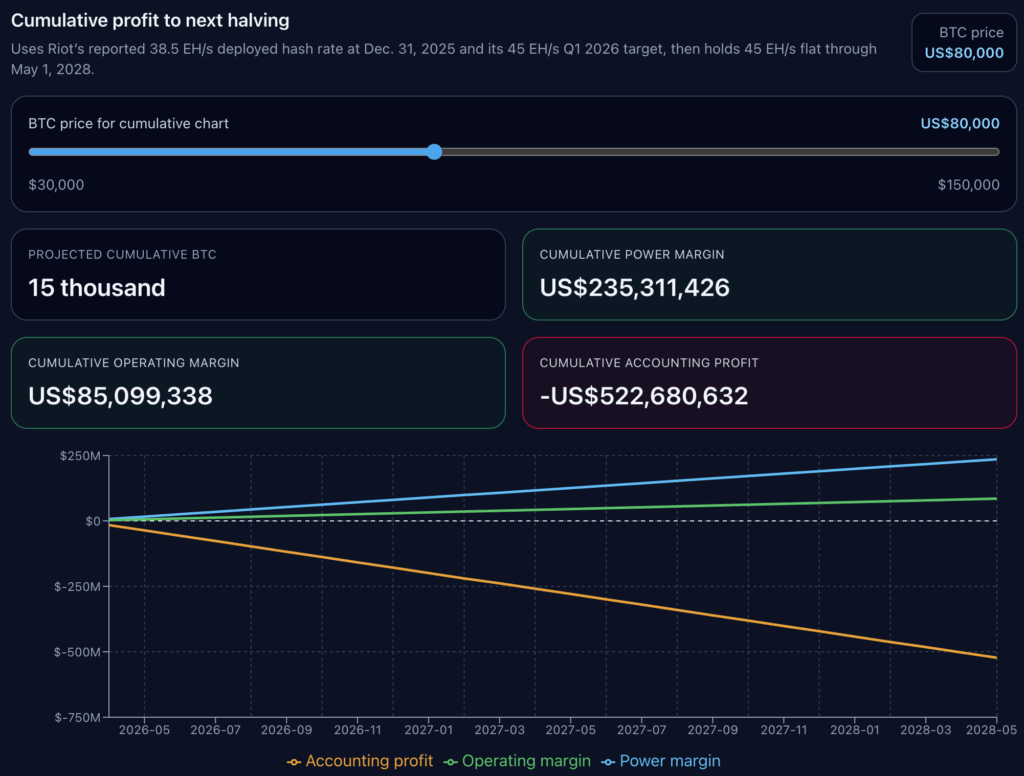

Using Riot’s latest public documentation, assume that 38.5 exahashes per second increases to 45 EH/s by March 31, 2026, and then maintains that level until the next halving.

We’re not trying to rebuild the entire market. The model remains up to date.$BTC The economics are constant and scale through the self-mining hash rate path that Riot is reporting and planning.

This is a scenario exercise focused on operating leverage, and price sensitivity is hard to overlook.

Expected cumulative across all four scenarios $BTC Mining is 15000. What changes is the profit stack.

At $49,000 Bitcoin, Riot’s cumulative power margin is negative $239,436,036, cumulative operating margin is negative $389,648,124, and cumulative accounting profit is negative $997,428,094.

At $67,200, the cumulative power margin becomes positive at $39,286,667, but the cumulative operating margin remains negative at $110,925,420, and the cumulative accounting profit remains negative at $718,705,391.

At $80,000, Riot has a positive operating margin of $85,099,338, but its cumulative accounting profit is still negative at $522,680,632.

Only in the $126,000 scenario are all three lines above zero, resulting in a cumulative accounting profit of $181,783,343.

Although miners can maintain power plus for long periods of time, it may still not cover a wide range of operational costs. Furthermore, even if operating income turns positive, it may still be far from accounting profit. The Riot case study shows the wide disparities between these states.

In this model, the difference between the electricity breakeven point and the fully accounting breakeven point is approximately $49,495 per case. $BTC. This spread helps explain why miners look healthy in fleet dispatches, while at the same time taking a toll on reported revenue.

Our cumulative charts do not take into account future hardships, fees, outages, reductions in income, financing, or new capital expenditures. I’m assuming it’s around today.$BTC The economics last and only scale according to Riot’s planned hashrate path.

This restriction still leaves a clear signal. Holding the rest of the economics flat shows how much of the debate about the next halving still hinges on Bitcoin price.

For Riot, this model does not reach cumulative accounting revenue until the $126,000 scenario is reached. However, in absolute terms, the level is $114,200.

Riot case has new implications for the entire U.S. mining trade

The broad lesson for U.S. miners is simple and clear. Price alone does not determine business conditions. The initial reduction still depends on vehicle efficiency and electricity prices.

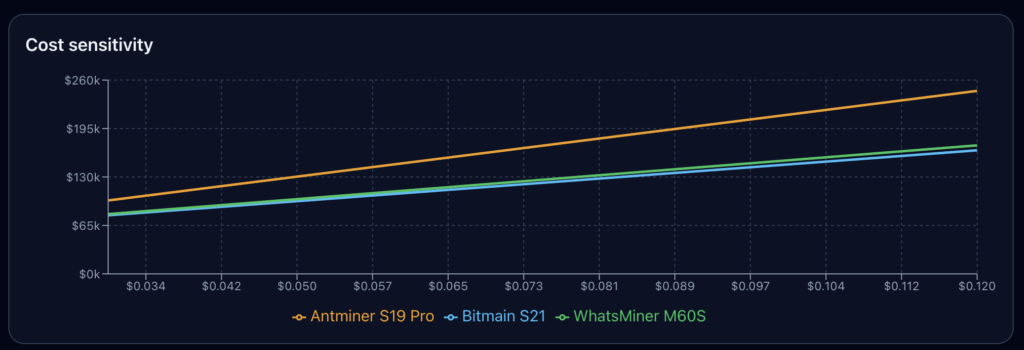

From a cost sensitivity perspective, we compare three ASIC presets: Bitmain S21 at 17.5 J/TH, WhatsMiner M60S at 18.5 J/TH, and Antminer S19 Pro at 29.5 J/TH using the Texas Industrial Power Reference Rate.

Across its range, the S19 Pro outperforms new machines on cost per unit. $BTC. Although the two new models operate close to each other, the less efficient vehicle shows a visibly higher cost line across the graph.

In that respect, it exceeds Riot. Riot’s declared non-power cost tiers and depreciation assumptions are company-specific. Different miners may have different overhead bases, different lifetime assumptions, different reduction profiles, or different realized power configurations. However, I feel that the three-layer structure still flies well.

First is the electricity cost. Next is operating costs. Next is accounting costs.

Companies that survive periods of low stock prices tend to pass the first tier easily. Companies that grow value through cycles need to do all three over time.

At a current price of about $67,000, this model does not indicate that the company is in trouble at the machine level. Power margin is positive. Machines still make more money than they spend on electricity.

At the same time, the miners who have solved the complete income statement are not shown. The motion line remains red. The fiscal line remains in even deeper deficit. For public miners, this split will determine Treasury decisions, when to replace vehicles, and market expectations for revenue.

Therefore, we can speculate that Bitcoin miners could reach positive power margins well below six digits, positive operating margins in the recovery case, and still miss out on cumulative accounting profitability until we retest the all-time high above $114,000.